China Automotive Systems Is About to Report Its 2025 Full-Year Financials, The Previews Are More Interesting Than Expected

There is a specific type of business that works hard but receives very little recognition for it. For...

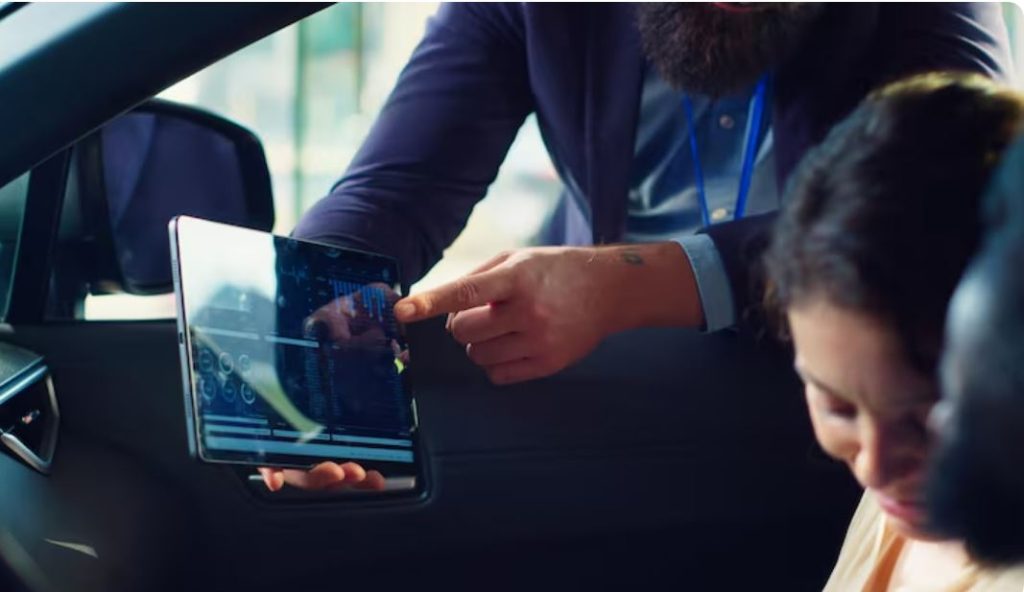

These days, you notice a certain kind of silence at car dealerships. Something quieter was taking place inside the laptops on the finance manager’s desk, rather than the showroom hush of polished hoods and brochure racks. A credit decision that once required three coffees and two phone calls is being shaped in real time behind the screen by systems that the majority of customers will never see. Sitting somewhere in that silence is Genpact, the professional services company that has spent years integrating itself into the back offices of international banks and automakers. Additionally, its mobility finance model—which it has been honing with partners like Volkswagen Financial Services—is beginning to reshape the auto loan experience in ways that the sector has been promising for ten years but has hardly ever fulfilled.

On paper, the pitch sounds familiar. excessive personalization. omnichannel support. quicker choices. The vocabulary is familiar to anyone who has read a fintech press release in the past five years. Perhaps the execution is different. The question is no longer whether auto finance companies are adopting AI, but rather how awkwardly or smoothly they are integrating it into the actual workflow, according to a recent industry report released by Genpact’s own executives. The majority are still awkward. Some are doing it correctly. There’s a feeling that the distance between those two groups will soon grow significantly.

Think about what the customer sees—or rather, what they are no longer required to see. The lengthy process of filling out forms, the days spent awaiting underwriting, and the uncomfortable follow-up appointment to sign paperwork are all undermined by Genpact’s methodology. Their multilingual generative AI tool, Cora Knowledge Assist, is integrated into VWFS operations and responds to customer inquiries with a speed that previously required a senior agent and a thick binder. Depending on how a conversation is going, their Cora Nudge Coach suggests tone changes or product matches to human agents in the background. The client might not even be aware that any of this is taking place. In a way, that’s the point.

What occurs prior to the customer entering the store is more difficult to observe, but it may have greater implications. 56% of auto finance customers were not entirely satisfied with their experience, according to Genpact’s own 2024 customer experience study from Germany, despite the fact that 61% had voluntarily provided personal information in the hopes that it would be used to customize something for them. The fundamental flaw in conventional auto lending is this contradiction—the data provided but never returned in the form of improved service. By viewing the customer journey as a single continuous data thread rather than a sequence of interconnected stops, the mobility finance model attempts to address this issue. Retention, vehicle remarketing, sales, and servicing all contribute to the same overall picture.

This is part of a larger cultural change. In contrast to their parents, younger consumers do not wish to own automobiles. Pay-per-use, shared fleets, and subscriptions seem specialized until you consider how many drivers under thirty in Germany and the Nordic region already use them. Auto finance firms that relied on balloon payments and five-year loans are quietly losing market share. Genpact essentially argues that becoming a mobility provider instead of a lender is the only way out. It’s still unclear if the industry is prepared to take that step.

It’s difficult to ignore the fact that the fastest-moving companies aren’t the loudest. The VWFS collaboration treats AI like plumbing rather than promoting it as a destination. In the end, that’s probably what alters the customer experience more than any glossy demo. The old car loan isn’t going away very quickly. While everyone is searching elsewhere, it is simply being gradually replaced, one workflow at a time.

There is a specific type of business that works hard but receives very little recognition for it. For...

When an industry consistently delivers on its promises, a certain kind of weariness descends upon it. That fatigue...

You’ll notice something strange if you walk into a Hyundai dealership on a Saturday afternoon in a suburban...